During the peak-season before the Lunar Chinese New Year (Feb 1) holiday, hiking sea freight from China to Southeast Asian nations nearby added some fire to the hot marine market which has been disrupted by the pandemic.

Southeast Asia route:

According to the Ningbo Container Freight Index, the freight of Southeast Asia route hit historic high in recent one month. The freight from Ningbo to Thailand and Vietnam surged by 137% from end-Oct to the first week of Dec. Reflected by some insiders, the freight of one 20-foot container from Shenzhen to Southeast Asia has hiked to $1,000-2,000 now from $100-200 before the pandemic.

It was reported that Southeast Asian nations were resuming production and showed recovering demand for materials. Many shipping companies focused on trans-Pacific route since the third quarter as export demand was expected to be huge due to the Black Friday and Christmas Day. As a result, short-distance shipping space was tight. The congestion of ports in Southeast Asia is estimated to sustain in short term supported by booming shipping demand.

Looking at the way forward, some industrial insiders thought Asian trade is anticipated to embrace a new era as the RCEP will be come into effect.

European route:

Europe was the area where Omicron variant was discovered earlier. The spread of pandemic worsened apparently. Players’demand for the transportation of various goods sustained high. The shipping capability was largely unchanged. With stricter regulation at ports, the congestion remained. The average utilization rate of seats at Shanghai port was almost near 100% recently, with stable freight. As for the Mediterranean route, the average utilization rate of seats at Shanghai port was around 100% amid stable transportation demand.

North America route:

Many Omicron variant infected cases emerged in US recently with the daily new infections of COVID-19 pandemic exceeding 100,000 again. The spread of pandemic was serious now. Players showed high demand for various commodities including the pandemic prevention materials. The stagnated of containers and the congestion at ports caused by the pandemic kept serious. The average utilization rate of seats in W/C America Service and E/C America Service was still near 100% at Shanghai port. The sea freight kept high.

Western ports in the United States include Los Angeles/Long Beach, where delays and congestion remained severe due to labor shortages and land-side traffic problems, container stagnation and poor transport turnover. There has been a marked increase in the number of blank sailings between Asia and the United States, with an average of 7.7 suspensions per week in the first nine months of this year. On December 6, the ports of Los Angeles and Long Beach announced that they would postpone the collection of “container overstay fee” from shipping companies for the fourth time, and the new charge was tentatively scheduled for December 13.

The ports of Los Angeles and Long Beach further indicated that since the announcement of the charging policy, the number of containers stranded in the ports of Los Angeles and Long Beach has decreased by a total of 37%. In view of the fact that the charging policy has greatly reduced the number of stranded containers, the ports of Los Angeles and Long Beach decided to postpone the charging time again. Port congestion is a global phenomenon that causes serious delays and forces carriers to onmint ports, particularly in Europe, while imports from Asia are expected to remain strong until late-Jan. Port congestion has delayed the shipping schedule, so the capacity has been shelved.

Carriers may encounter increasing suspension of shipping and onmint of ports among the trans-pacific trade in Dec. Meanwhile, shipping companies may skip over the ports in Asia and America to resume the shipping schedule.

According to the latest data released by Drewry on December 10th, in the following four weeks (week 50-1), the world’s three major shipping alliances will cancel a number of voyages successively, with the THE Alliance to cancel the most 19 voyages, the 2M Alliance 7 voyages, and the OCEAN Alliance 5 voyages at least.

So far, Sea-Intelligence predicts that trans-Pacific routes will cancel an average of about six schedules a week in the first five weeks of 2022. As time approaches, shipping companies are likely to announce more blank sailings.

Market outlook

Some industry insiders said that the previous decline in shipping prices did not mean that the export scale will weaken in short term. On the one hand, the price drop was mainly reflected in the secondary market. In the primary market of container freight, the quotations of shipping companies and their direct agents (first-class forwarders) were still strong, still much higher than the level before the pandemic, and the demand on shipping market as a whole remained strong. On the other hand, since September, supply of global shipping has gradually improved and formed a certain support for exports. Players expected this improvement to continue, which was an important reason for the price reduction of freight forwarders in the shipping secondary market.

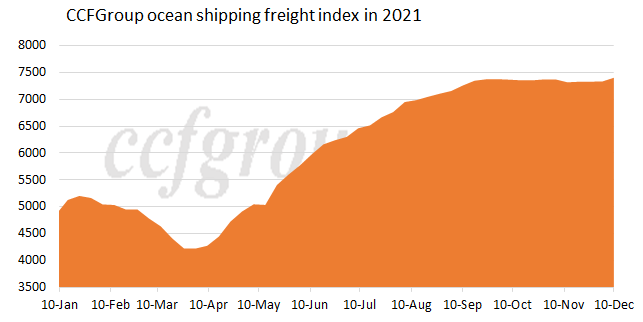

Reflected by the latest data, freight index extended higher, which indirectly echoed good demand on container marine market. The congestion of ports has eased but demand for container marine transportation sustains high. In addition, the appearance of Omicron Variant intensifies the worries on the recovery of global economy. Some market players expect freight to sustain high impacted by the deteriorating spread of the pandemic in short run.

The Moody’s lowers the outlook for global shipping industry to be“stable”from being“active”. Meanwhile, the EBITDA of global shipping industry is estimated to reduce in 2022 after outperformed in 2021 but may be still far higher than the pre-pandemic level.

Some players expect container marine market to remain stable and robust but the situation is unlikely to be better than it is now in the following 12-18 months. Daniel Harli, Vice President and Senior Analyst of the Moody’s, expressed that the income of containerships and bulk cargo ship both hit record high but it may reduce from peak and keep high. Based on the data from Drewry, the profit of container marine market is expected to hit record high at US$150 billion in 2021, which was at US$ 25.4 billion in 2020.

The shipping scale of the previous global top 5 liner companies only accounted for 38% of the total in 2008 but the proportion has surged to 65% now. According to Moody’s, the integration of liner companies is helpful for the stability of container marine industry. The freight is estimated to remain high in expectation of limited delivery of new ships in 2022.

From Chinatexnet.com

Post time: Dec-16-2021