The bell of the New Year is about to ring. Looking back at in 2021, repeated pandemic causes, soaring raw material costs, and China’s dual control policy on energy consumption, nylon industry chain has been impacted in turn. The pressure on business operations is not negligible, and the competitive pressure in the chemical and textile and chemical fiber industries is inevitable. The game between upstream and downstream, peer competitors has always been very fierce.

But what is pleasantly surprised is that at the end of the year, CPL and chip plants have been running smoothly with a relatively high operating rate and relatively ideal profit margin, which may continue until after the Spring Festival.

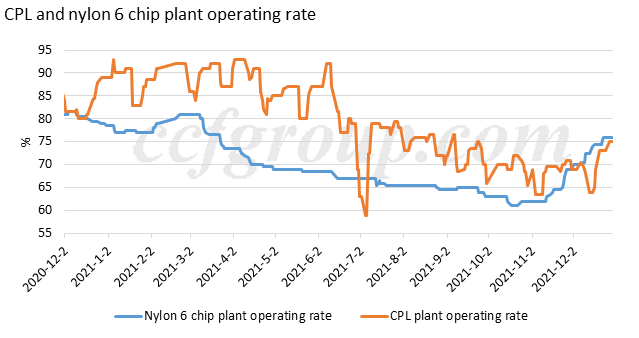

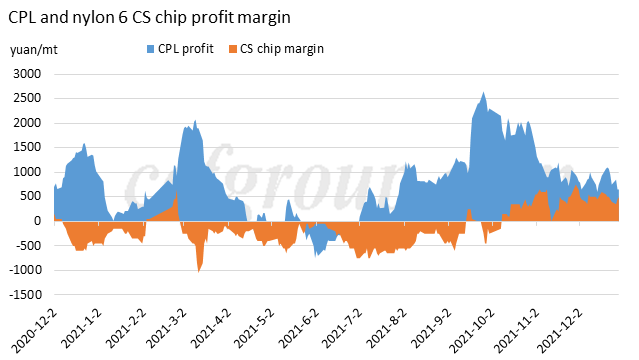

CPL and chip plants maintain low stock, high run rate and high profit by end-2021

We have mentioned in the insight report“CPL & PA6 enter rebalance toward end-2021”published in end-November that CPL and nylon 6 chip plants would continue raising their operating rate and the supply-demand pattern will enter into a rebalancing period. Over one month, the actual operation of CPL and nylon 6 chip plants have proven this trend, and surprisingly, both CPL and chip inventory are kept low, and the profit margin in CPL and nylon 6 chip links are still good.

There are two reasons underpinning the above result.

First, chip downstream mills had been holding a minimum of polymer stocks in November, and they were restocking more actively in December, when the market hit a bottom low and rebounded and chip plants ramped up operating rate.

Second, CPL plant operation was not smooth in December. Major suppliers including Luxi Chemical, Hualu Hengsheng, Hubei Sanning and Sinopec Baling Hengyi took turns to shut or cut production in the month and caused a tight balance in CPL market.

High operating rates:

The above chart shows the operating rates of CPL and nylon 6 chip plants, which have both been rising evidently in November-December 2021.

CPL plants are now running at the average rate of 75%, which is not a high rate in history. However, considering that the of Haili Chemical (400kt/year), Inner Mongolia Kingho (100kt/year), and Sinopec Shijiazhuang Refinery (100kt/year) have been shut due to force majeure, and most of other plants are running at relatively high rates.

The run rate of nylon 6 chip plants has been rising significantly throughout November and December, up from 61% to 76%, mainly as nylon 6 conventional spinning chip plants have elevated their average run rate from 57% in end-October to 79% till end-December, and at the same time that of nylon 6 high-speed spinning chip plants have moderately raised from 66% to 73%.

High profit margin:

Caprolactam producers have enjoyed abundant profits in the second half of the year as the price spread with benzene enlarged continuously.

As discussed in the previous insight“Lucrative profit of nylon 6 CS chip sustainable or not”, nylon 6 conventional spinning chip suppliers have been enjoying lucrative profit in the fourth quarter of 2021. Nylon 6 high-speed spinning chip plants’margin is relatively steady due to the stable processing margin based on CPL contract settlement.

Before the CNY, CPL may sustain tight balance, price trend keeps resilient

Based on the above mentioned situations, we are looking forward to the Spring Festival (end-January to early February).

First, based on the low stock and high profit, nylon 6 chip plants may continue high operating rate and restock CPL moderately in January 2022. There are still some uncertainties around the holiday, like stock management, price fluctuations after the holiday and demand under the pandemic. But the operation strategy of polymer plants is quite certain so far, that they would keep running at least at current high rate, and they would like to replenish caprolactam before 2022 Spring Festival, as the Beijing Winter Olympics and cold weather in North China may limit down CPL production and logistics. In order to ensure feedstock supply, polymer plants are likely to prepare enough CPL before mid-January.

In addition, if nylon 6 chip plants’operating rate is pegged at 76%, and CPL plants keep running at around 78%, CPL market is still under tight balance given their effective capacities. So it is hard for CPL inventory to accumulate.

Second, upstream crude oil and benzene market is in a bullish period, and even there is downward pressure from ample imports of benzene in January, it may not burden down benzene price too much. A moderate decline in benzene may not trigger down CPL market, which is on a good fundamental.

Third, from the mentality perspective, previous bearish influence is reducing. The decline in CPL during October-November 2021 was to a certain degree influenced by the news of upcoming new capacities, which affected players’mentality at that time, particularly before their supply was released. But after a period of operation, the products from the new plants have gained steadier quality and proper pricing position in the market, and its influence on the mentality is reducing. From this point of view, the bearish influence of CPL new capacities are falling down.

So sum up, CPL market may sustain a high profit and low inventory status before the 2022 Spring Festival, and it may provide a solid base for downstream polymer market.

From Chinatexnet.com

Post time: Jan-04-2022